Chapter 16

ANALYSIS OF THE RESULT

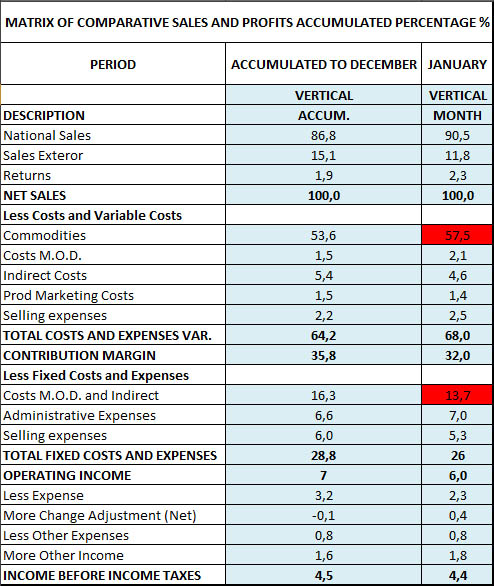

STATEMENT (example)

The aspect of great importance practical to obtain the objectives of value generation is the periodic analysis of the earnings statement (generally every month) to be evaluated as an advance in the annual exercise in terms of working days and making decisions logics, oriented to the continuous improvement.

For it, he is very recommendable to have a comparison pattern, which takes shape with two parameters that are to say: the earnings statement of the previous exercise (where we are) and the projected one for the exercise in the course (to where we want to arrive) in agreement with the strategic planning. For both cases, a vertical analysis is fundamental in that it indicates the participation of each one of the debts as a percentage of the income and allows us to make questions to the games that do not obey logic.

If for example, the expenses of sales for the previous period are equivalent to 13% of the sales, because they are going to represent 7% in this one accumulated period or the month that we analyzed?

This type of question is taking to find a logic to us to accept or to reject a number that leaves normal conditions unless an acceptable explanation appears to reason, why is very recommendable to both, compare the results of the month in the study with parameters, being done emphasis in the accumulated period. For it is important to consider the following considerations:

Accepting the difficulty practical of the accounting to accurately measure the results of a company (unless very a well-designed software is used) and the urgent necessity to know the advance the business to take actions from improvement, he is advisable to understand, of the best possible way, which indicates the earnings statements with their factors of vagueness to be able to analyze them and to take advantage of better the information than they provide.

The accounting, according to the principle of the countable period, divides the existence of the company in annual days to the aim of which the financial statements appear officially basic.

For administrative effects, we disturb the year in monthly periods and the earnings statement is prepared to evaluate it and to take remedial actions.

Before accepting the game of utility or loss of a month in relation to another one, we must be careful with the following eventualities that can be presented/displayed, among others:

INCOME

-

Dates of closing. It is very common that the people in charge of sales slow down the countable cut looking to present/display better numbers. In this one case, the entrance is had but the costs and fixed expenses of the days are not entered that extend the invoicing, besides accelerating the payment of the part corresponding to the IVA.

-

The quantity of sales returns can be presented/displayed that correspond to periods previous to the month at issue. By all means, the entrance is increased to the low cost and.

-

Discounts by any circumstance, that they do not correspond to the effective sales of the analyzed period; the effect is he himself of the previous numeral.

-

The working days of the month. If beforehand we know that the year presents/displays a certain number of holidays, months have but “relative steady load” without being able to generate income in the non-working days.

- Production available to invoice and not dispatched; of this one form one does not register the operative utility, but the fixed costs and expenses; like an obvious consequence, the utility is not registered.

DEBITS

-

Variable costs. They can be seen affected by changes in the prices of raw materials that do not necessarily appear in the period that is analyzed. For example; raw material increases in price in January, enter to modify the cost average and it is used in March; the effect also can be negative. Of the same form, a change with any other variable component can be presented/displayed.

-

Hidden Costs1. They represent another cause, sometimes the one of greater impact on the results. As its name indicates it, they constitute a true challenge so that the administration reduces them to the maximum. The important thing is to identify them and to quantify them, expressing them like a percentage of the sales, an indicator that must try to be reduced to its minimum expression.

-

As far as the fixed costs and expenses, the phenomenon is more critical because of those non-working days. of all ways imply the corresponding payments without there are production nor sales. The same happens with the financial expenses, which appear as it spends the time.

-

The handling of the provisions, estimations calculated with the inherent uncertainty by its character of so, that they can affect positively or negatively the result. For its handling, prudence is recommended.

-

In addition, the units sold in the month not necessarily are the produced ones (or bought) in him himself, and therefore the cost of the produced merchandise is not just like the cost of the sold merchandise.

The previous analysis causes that inconsistencies in the results appear, independently of the quality of the management that is fulfilled, simply by imprecision in the handling of the headings of income and debts to register. These considerations allow us to suggest the convenience of the cumulative analysis which will be more representative of the reality in the measurement that advances in the exercise until arriving at the end of the annual period when the inventories and the provisions conciliate with rigor.

The handling of the numbers of the period (as many years, as months) expressed in terms of working days is recommended, dividing the accumulated total by the number of days thus to calculate the results of the exercise object of the analysis inconsistent form and first of all, to avoid all the distortions of information with explanatory notes.

The previous annotations are very useful for the elaboration of budgets and the periodic control-oriented to the decision making and remedial action based on information that comes near to the real scenes and fulfills their assignments like a tool of value generation and continuous improvement.

Note: it is recommended to structure a committee that analyzes and reports monthly on the behavior of hidden costs, which result from situations of common occurrence due to lack of concentration and communication such as errors in assemblies, sudden changes in the order of the process, machine damage due to lack of preventive maintenance, poorly taken orders, production schedules not consistent with the possibility of dispatch (portfolio problems, transportation logistics, etc.), use of inappropriate materials, poor quality, in the vast majority of cases, due to carelessness and lack of commitment, work accidents, any other anomalous situation that involves loss of time affecting the level of production, deterioration and inventory losses for any reason.

Concept of AI: The article by José Saúl Velásquez Restrepo provides a detailed and well-founded vision of the importance of strategic planning in companies. Some of the key points are summarized and discussed below:

SWOT Matrix: The author highlights the usefulness of the SWOT matrix (Weaknesses, Opportunities, Strengths and Threats) as a practical and analytical tool in strategic planning. This matrix is widely recognized for its ability to evaluate both internal and external factors in an organization.

Focus on results and value generation: The article emphasizes that strategic planning finds its true meaning when it translates into measurable results and satisfies the expectations of various stakeholders. The generation of value for society, customers, employees, suppliers and shareholders is a central objective in strategic planning.

Planning levels: Different levels of planning are mentioned, from Vision and Mission to Tactics and Programs. The articulation of these levels is essential to achieve effective implementation of the strategy.

Culture of innovation: The author highlights the importance of promoting a culture of innovation in companies. It is recognized that innovation is not limited to products only, but can also manifest itself in ideas and practices in all areas of an organization.

Leadership and leader skills: The article mentions the qualities that leaders must have in the strategic planning process. Empathy, the ability to guide and motivate teams, and fairness in decisions are essential characteristics to successfully lead the implementation of strategies.

Schedule and prior preparation: The importance of a schedule of activities and the assignment of responsibilities in the preparation of the strategy is highlighted. This planning stage is crucial to ensure the process is effective.

In general, the article offers a complete vision of strategic planning and its importance in companies. It highlights the need to align the strategy with the generation of value, the importance of the culture of innovation and the fundamental role of leadership in this process. Furthermore, it emphasizes the need for careful preparation and consideration of hidden costs in the strategic planning process.