Chapter 3

FINANCIAL INFORMATION FOR ANALYSIS AND DECISION MAKING

The phenomenon of globalization is irreversible and the great development of electronic banking and the Internet make easy the actions of investors, whether it be permanent or tern- capital to universal accounting standards (IFRS) will tender much their decisions.

Even for self-management, it is desirable that all people, regardless of their trade or profession acquire basic financial knowledge to facilitate their investment decisions, either as entrepreneurs in private businesses, regardless of the type or size of the company, or investors through the financial system. The concept is valid, more so in the case of professionals linked to companies, regardless of the function that they perform, by the urgent need to achieve productivity, forcing judiciously prepare plans for value creation involving all executives for survival in a highly competitive environment, which urgently take the companies to implement risk wage based on the results obtained, which makes it a fair compensation model for shareholders and employees, including the management team contributing to an enterprise system to actively participate in sustainability with more social justice.

In the modern world is taken for granted in order to improve the quality of life and is beginning to use the happiness index as the most important country-level indicator.

Although seemingly very abstract is a challenge for the social sciences to refine the model so that it is a generally accepted index and becomes a target level of countries and companies in general because there is a direct correlation between the level of happiness and productivity. People working happy are very creative, innovative, and efficient.

To get the level of satisfaction the basic needs human is related easy; continues with more complexes or higher-order for the achievement of the competition of the other is required, which lead us to pose as business objective the pursuit of happiness as a contagious group of integrated groups with people of great personal qualities.

Of course, you cannot talk about happy groups if they don´t have comfortable working conditions with good landscaping and other environmental amenities. As people usually work the third of the day, it is necessary that the governments address sustainability and regulate all relevant charged applicable taxes and administer with absolute TRANSPARENCY exterminating corruption so that the money provided by the companies is fully implemented to create inclusive environments that protect families like the cell of society and help catapult the degree of happiness to increase personal happiness, productivity base to compete in a globalized world

In this vein, there is a big gap between the administration and accounting. On one side all the advanced administration agrees that human resources are the most important and spare no efforts in recruitment, training, development, and compensation, including the family.

To the extent that teams well integrated with people of great quality personnel (business rates) are taken, solidarity, life plans consistent with business organization, and duly committed to the mission and vision of the company an intangible asset is achieved valuable amounts to a significant proportion of intellectual capital. It is complemented by investments in ENVIRONMENTAL SUSTAINABILITY AND INNOVATIONS; explains much of the difference between the market value of the stock and its intrinsic value.

To achieve these levels of intellectual capital, companies require large investments accounting usually treated as reducing profit, and therefore paying fewer taxes, but creating hidden reserves that need to be kept when calculating the value of the company.

This document is intended to facilitate understanding of the financial statements to the accounting system that has been developed with a very simple language to make it accessible to all.

The accounting system has developed a consistent framework for analyzing companies of different types of activity governed by accounting principles models and some international accounting standards (IFRS ) that are imposed because of globalization and irreversible phenomenon Each country to regulate its own model and unique charts of accounts for the different sectors (PUC ) must comply with the IFRS to be consistent with international systems, which greatly facilitates negotiations with the outside and prevents adjustments to run countries that have not yet done.

Accounting information must reveal comprehensively the economic events affecting the financial position of the company in an understandable and useful to meet international goals, which is achieved with well-ordered figures, classified according to the PUC, compared with an initial situation, supplemented by explanatory notes and the directors' report to be submitted by the manager and the board at the meeting of shareholders must necessarily celebrate at end of the year to track progress or reverse situations where they appear and as a guide for the distribution of dividends, business valuation for legal purposes and other strategic decisions.

Financially speaking, their predictive power is very poor, because they correspond to the past and show the result when the real financial function points to the future. As executives must act ethically and with full responsibility to them for their position, it is essential to go creating a culture of informed projections, beginning his presentation comparing actual results with budgeted. They should make a careful analysis of deviations, which is a powerful tool for the objective evaluation and feedback of experiences; also provides a basis for the implementation of wage risk managers, who must have an income that allows them to live in dignity and at year-end compensation linked to the result as with shareholders.

Ideally, investors can compare the expectations of the company with others available on the market and the comprehensive analysis is provided in the stockholders to provide all of the same information are aware of the strategic plan and discuss and approve the distribution of dividends, consulting the state income statement and the project cash flow or that others call the free cash flow projected.

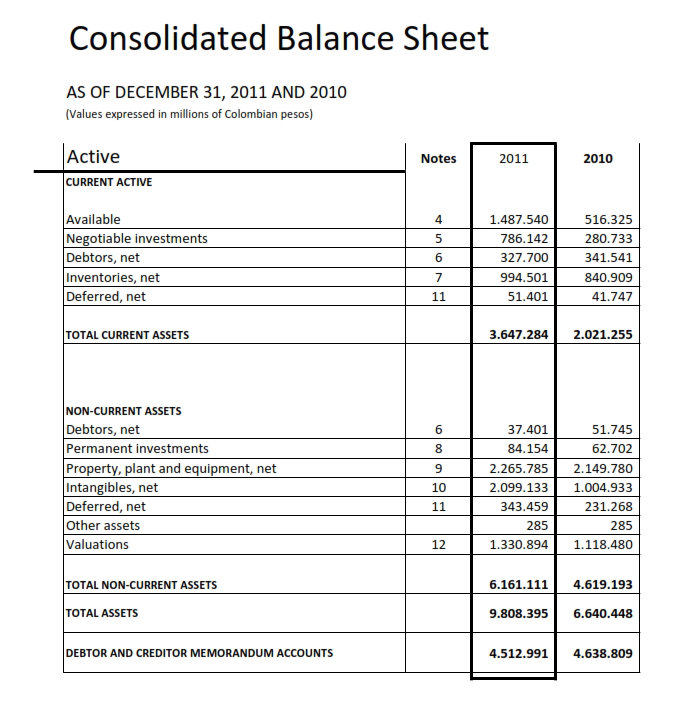

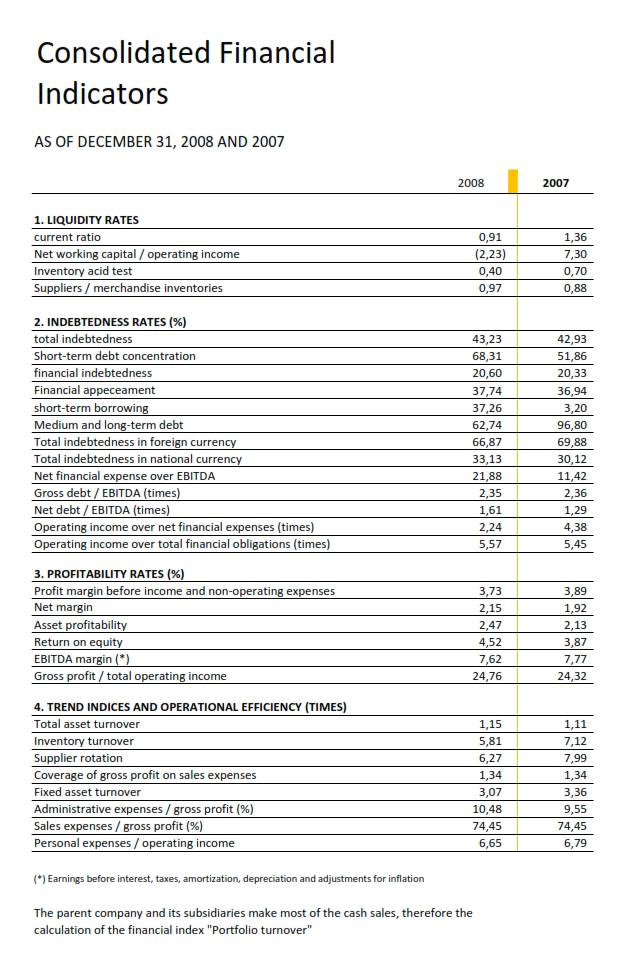

We will take as a guide the content of these consolidated financial statements, Group EXITO (warehouses and subsidiaries) duly certified by the auditor. Complete information is available online

The balance sheet

The balance sheet and other financial statements are part of the report present management's prior review of the audit and tax inspection certificate by sharing the ethical and legal responsibilities of both the numbers and the additional notes must be submitted with the indicators of value creation, liquidity, activity, debt coverage, and profitability. It must be available for all shareholders to avoid information asymmetries as required by good corporate governance practices.

In simple terms, a balance equivalent to the equation: A = P + Pat (total assets equal total liabilities plus equity) at a given date to be timely, just completed the exercise to evaluate and verifiable figures which indicates that you must faithfully represent the economic events.

The assets, which are generally in the left column, valued according to the NIIF in domestic currency are characterized by identifiable; the company must have a power of control over them and they must also have the potential capacity to generate cash through a well-run business because no active, alone, produces income.

They are classified into two basic groups: Fixed and Currents; they can also be exhaustible, and other intangibles (deferred charges as ongoing constructions, installations, and assemblage.

The sum of them all is the total assets, which should be valued in accordance with IFRS consistently, keeping the method used throughout the life of the business, unless a change is required, in which case, you should leave a clear note explaining why and its effects.

A) Non-current assets are fixed or infrastructure; assemblage that is required to perform the operation and includes no -depreciable land and depreciable or amortizable other buildings, machinery, equipment and tools, vehicles, patents, licenses, and other operating that are not to be sold but to be used. Usually grouped into:

1) Property, plant, and equipment generally are valued at acquisition cost more improvements, additions, capitalizing on an exchange, and other financial expenses attributable to acquisition plus inflation adjustments. The above figure is the basis for calculating book depreciation, which reduces the value of the asset and is calculated with the following basis:

5% of value for buildings, equivalent to 20 years of useful life

10% for machinery and equipment, equivalent to 10 years of useful life.

20% for vehicles (equivalent to 5 years lifetime).

For other real flexible or accelerated depreciation in cases of rapid obsolescence as computer equipment or based on hours of work may be used attending technical specifications of the supplier.

It can also be based on replacement value, market value, commercial appraisals, or the discounted present value according to the NIIF.

Subsequent improvements can be capitalized as a greater value of the asset or handled separately if it is probable that future economic benefits are obtained. Valuations directly affect the heritage.

2) Deferred assets and prepaid expenses such as interest and insurance to be amortized as cases such as the benefits and improvements to the property are received, while exploits, construction in progress, temporary tax differences when you have reasonable expectations reversal.

They can also represent goods or services which are expected to receive economic benefits as project development, software, and advertising and promotion expenses, including adjustments for inflation.

3) Intangible assets, amount to direct expenditures incurred to acquire trademarks, distribution rights, lease -purchase, research and development, goodwill, and certifications that correspond to clearly identifiable expenses and amortized annually.

In the case of trademarks and patents, valuation should be based on technical studies conducted by an investment bank to determine the payback time; in leases with the option to purchase, assets and liabilities are recorded at the present value of the fee and agreed purchase option, calculated from the date of commencement of the contract based on the internal rate of return of the respective contract and rights are amortized using the straight-line method under the income statement as interest expense.

The research and development expenditures are recognized as intangible assets when the product or service is developed or improved technique to achieve commercially viable and economic benefits. Here is amortized linearly; otherwise, it is treated as an expense that affects the income statement.

The certifications: ISO 9000 Quality, ISO 14012 Environmental, safety BASC trade, security and OHSAS 18001 occupational health and good manufacturing practices and HACCP, BPM recorded by the total investment to get them.

Goodwill is the additional amount paid over the book value to acquire shares in companies in which the parent has or acquires and amortized over time to be recovered, not exceeding twenty years.

B) The current assets are accounted talking cash and other assets susceptible to becoming cash in less than one year or in an operational cycle like temporary investments, accounts receivable, and inventories.

To operate efficiently, the company requires minimal items in current assets, depending on the time of the operating cycle (raw material purchasing, production, sales, and revenues in manufacturing companies; purchasing, sales, and collections in commercial companies). Such games cash, accounts receivable and inventories become fixed assets for financial reporting purposes; is corresponding to working capital. The excesses that occur in these areas represent overruns inefficiency either by improper handling of cash, poor portfolio management, or inventory management. In business, many such errors negatively affect the financial structure and usually go unnoticed committed.

Cash available (box more shortened term investments) is a well-defined and easy to verify figure; holdings to provision the contingencies that may arise meet the statutory standard; inventories may be valued according to the NIIF.

The proportion of each of these quantities with respect to total assets is the structure of assets that indicates the relative importance of each of them with special care to analyze the most representative as the portfolio in banks, inventory purchases available for sale in commercial enterprises, various types of inventories in manufacturing companies, and so on.

Financially speaking, the structure of assets must be related to the financial structure according to the principle of financial compliance: fixed assets and the fixed portion of current assets or working capital are to be financed with equity and long-term liabilities.

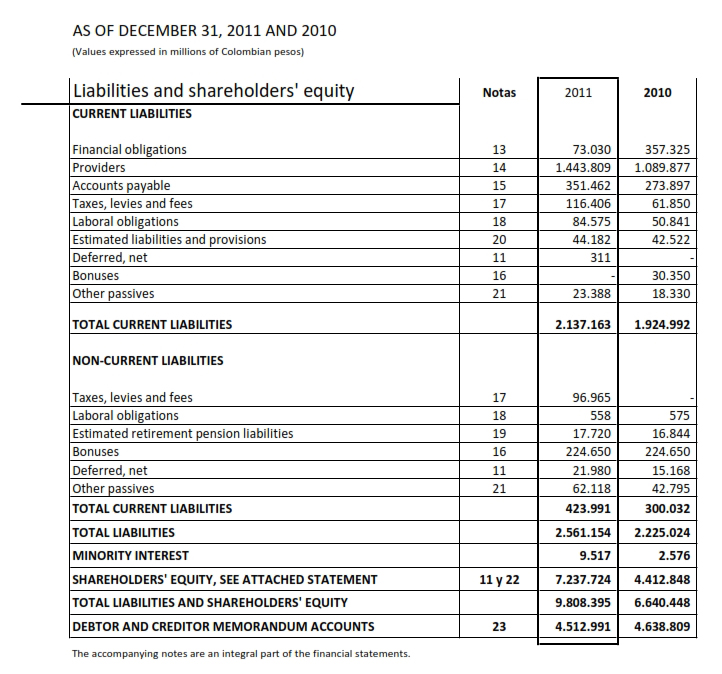

Liabilities

Represent a commitment to comply with a third party and are characterized by having a cost, due date, and a priority claim to the beneficiary in the event of a failure. They are classified into:

a) Current: characterized by having a maturity less than one year term and must be addressed financially with cash generation through the operation or the ordinary course of business;

b) Long-term, those with maturities greater than one year and equal to the difference between total liabilities and current liabilities. Among others, include financial bonds, and other employee benefit liabilities.

The sum of both is the total liabilities and the cost is calculated using the weighted average of all obligations that compose it and should be kept constantly updated.

1. THE EQUITY

that balances the two columns, in accounting terms, is the difference between assets and total liabilities; belongs to the owners, who are residual, in case of liquidation first serve other stakeholders namely government, employees, suppliers, and financial institutions.

It is for the owners of the company; your responsibility is to preserve and increase it harmoniously with attention to a social and environmental commitment by generating value, with good liquidity and trading facilities, which constitutes the main objective of the finance function. It is made up of contributions from partners, retained earnings from previous periods and exercise, the (legal and statutory) reserves, and revaluation surplus, the revaluation of assets, additional paid-in shares, and donations.

The value of equity divided by the number of shares outstanding is used to find the intrinsic value of the share, the basis for calculating Q (Tobin) which measures the ratio between the market value of the share and its carrying amount, allowing to estimate intangible assets, to the extent that the investing public is willing to pay a premium to acquire shares in the stock market.

The business world gives increasing importance to intellectual capital, which the human resource is one of the most important components and sustainable development, which is certified by specialized agencies; however, ignores the accounts, involving a very large void when it comes to valuing businesses and becomes a real challenge to the accounting system.

When a company invests in fixed assets, immobilizing cash and liquidity affecting as recommended; therefore fixed assets should be strictly necessary to meet the demand, with the expected development in the value creation plan, avoiding cost overruns from idle capacity, the opportunity cost of the capital invested.

Of course, the decision has to do with the type of business; sectors such as hydropower, transportation, hospitality, textiles, sports clubs, and others require very valuable structures, which in turn involve large outlays for interest expense, maintenance, and others that become fixed expenditures that increase the financial risk, forcing a search for cash generation, even sacrificing profitability, as do aviation companies, hotels, movie theaters when they have busy production plant. To properly use the effect should direct costing, the method is highly recommended for making decisions that help to surround the plant capacity

If instead, as is most recommendable financially, the structure is light, the financial risk is lower, but increases the operating risk; in this case, it is important to understand the current flagship asset, to find a high specialization in the dominant category as cash in financial institutions, trading stocks in the portfolio and the business type " trust you because I trust in you “.

Unless otherwise specified, it is assumed that the company has an indefinite life, but for administrative purposes, it is recommended to prepare papers and on the principle of accounting period balances, must be submitted for approval to the general meeting at end of year court to render objective and consistent reports of affected namely: government, workers, creditors, financial institutions and shareholders. These reports should be helpful to guide stakeholders with full disclosure.

The company, according to the principle entity is a separate entity from its partners in practice that is observed with a certificate of incorporation and management issued by the chambers of commerce and forces in their accounts any transaction with them.

The Balance Sheet and other financial statements should be complemented with indicators financiers considering its limitations and the action to be taken to make adjustments before the end of an analysis.

Liquidity ratios attempt to measure cash generation and ability to pay for short-term obligations and are commonly used EBITDA (operating income plus depreciation and amortization period), working capital, the current ratio, and the acid test tested and refined.

Activity indicators measure the length of the cash cycle, the time interval while investing in production or marketing processes to ensure the collection of cash and are calculated on the portfolio, inventory days, and the duration of cash cycle (days of inventory holding more days less day’s equivalent suppliers); are the essential complement to liquidity indicators. The shorter the cash cycle more liquidity and vice versa.

Debt indicators show the proportion and type of debt relative to total assets indicating the percentage that the court date, belongs to creditors in the event of a solution and evaluating the guarantees securing the various credits. It is required as a basis for calculating the cost of capital.

Coverage indicators measure the ability to generate cash to pay debt service; are indicators in terms of the time that disbursements are generated to cover existing commitments; are rather used by bankers and lenders. It is logical that the more times fixed charges of a financial nature are generated, the better the situation of the company.

Profitability ratios measure the efficiency from a financial standpoint profits relating to assets pledged assets used and relating them to the cost of capital in terms of whether it creates or destroys value.

In general, financial indicators complement the financial information has limitations but requires knowledge to make adjustments and relevant details before passing judgment as a basis for making a decision. If possible, it is recommended to take a series of seven statistical observations to prepare the Holistic Model that shows the trend and plot them to observe their behavior; to complete the diagnosis should be compared with indicators of other companies in the sector both nationally and internationally.

Memorandum accounts

According to the principle of prudence, are used as control and an administrative reminder to record events or circumstances that do not affect the balance sheet accounts and income but you should know its possible future effects such as consignment goods, issuance of stock obligations for contingencies (guarantees which are firms that guarantee obligations, disputes are resolved outstanding judgments, securities, financial derivatives). Create two: one of nature debtor and another creditor but do not represent anything in the balance sheet accounts or results ( assets, liabilities, capital, income, and expenses )

Consolidated financial statements

The groups must submit a parent company and other subsidiaries to group financial statements as if they were one company. The accounting policies and practices should be applied uniformly in the matrix or holding home and controlled. In the case of companies in different countries, prior adjustments are made for the consolidation is done with consistent information; to do this is necessary to proceed to eliminate intercompany transactions as sales and loans.

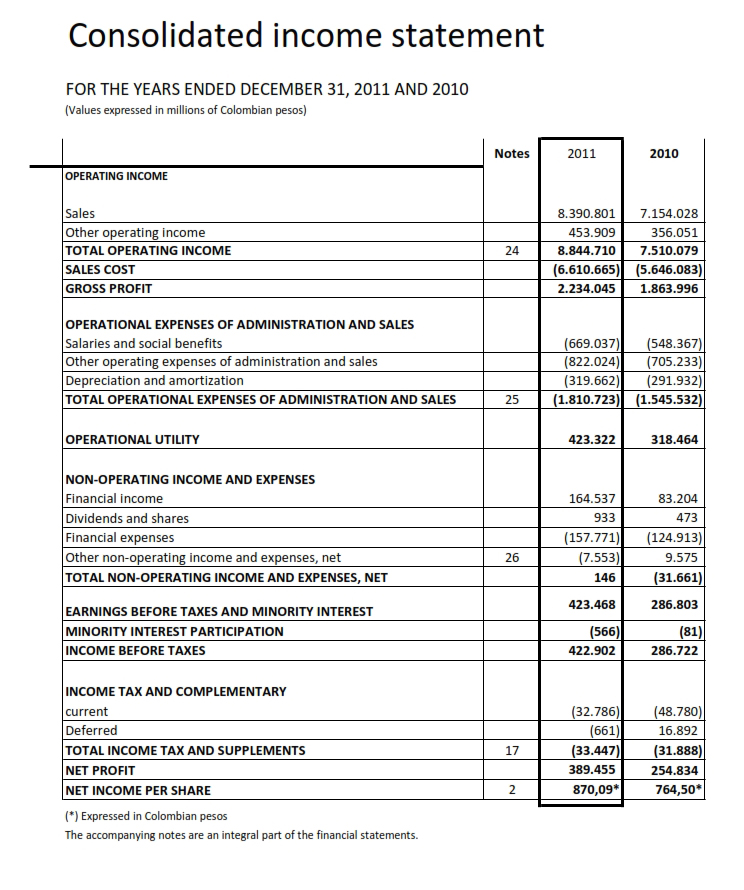

2. STATEMENT OF RESULTS

It is the tool to evaluate management in a period, especially with regard to the short term; measures the performance of the executive group and serves as the basis for calculating the indicators of activity, value, and profitability. Arithmetically speaking is the sum of revenues minus expenses diverse nature of all kinds. These are classified as extinct (non -cash items such as depreciation, amortization, and deferred expenses) and live (those involving cash outflows), a concept of great importance to calculate the break-even point, the level of production and sales support that allows the operation of the company with the cash it generates.

As the financial statements are aimed at decision-making, it is important to be aware of the limitations of the income statement as presented in traditional accounting; usually, income at the time sales are recognized, which on many occasions are made on credit, generating bills receivable are recorded as current assets on the balance sheet and strictly speaking, but do not generate income when the corresponding right I raise. It is also important to note that the profit is generated starting from the market research, continuing with the design, efficient production process with appropriate storage and packaging; is completed with the sale (at which accounting recognizes income) but is finished with the collection, without affecting the state results.

Some expenses are recorded before and go over the accounting periods as depreciation, amortization, and deferred expenses; others are made after passing the balance sheet as accounts payable and some are made in cash. Accounting gives them exactly the same treatment as if everything was done in an instant, forcing them to attach importance to the state of cash flows as a tool for measuring the liquidity and ability to pay. Therefore it is important to analyze carefully, with different optics, the figures before passing judgment, especially in companies that operate in countries with high inflation rates, which adversely affects liquidity.

Administratively speaking, it is essential to clearly distinguish the costs and expenses and fixed costs and variable costs concepts with which many conceptual errors committed appreciation. Fixed are presented in terms of time, regardless of the plant load factor and the degree of efficiency in the performance as depreciation, leases, payroll, and other fixed. The variables can be expressed in terms of a linear function:

y = f (x), is the sum of costs and expenses dependent on the level of production and sales. Costs are recovered through sales; expenses are not recovered.

Heading great impact on the income statement is the cost of sales, which is essential for the use of cost system suitable for the activity of the particular company because a wrong costing a company can lead to undesirable situations present with impact on cash flow, which if positive is good, even if they may affect sales, but otherwise it could lead the organization to technical insolvency, the most serious disease business. In the traditional format of the income statement ignored the hidden costs are common in all types of businesses and very easy to observe with the naked eye, which negatively affects the value creation and goes unnoticed without anyone assuming any responsibility for them.

In the income statement should be clearly differentiated operating income figures, emphasizing the vertical analysis by which the proportion of each of the components of cost relative to operating income for the year amounting to one hundred percent set (100 %) and compared with previous years and with budgeted figures in the value creation plan to serve as a basis for continuous improvement.

Due to globalization, a comparison of the cost variables with sector companies at both the national and international levels is necessary because, in the long run, market forces are imposed and a practical coping mechanism is increased productivity, measured in terms of real costs.

The achievements in the operative part cannot be lost due to underutilization of plant capacity " scheduled inefficiencies " , implying the SCO3 overruns calculable factor fixed costs associated with their occupancy, or overspending on the ground administrative, which can ruin the operational achievements as usually occurs in bureaucratic companies.

Nor can affect the results, via financial expenses that negatively influence and affect the final result. These depend on the general conditions (country risk) and mainly interest rates play an important role in the performance of the economy and are due to macroeconomic management; in particular, the financial structure of the company and its cash generation.

The income statement allows us to analyze such situations and check the times you win operatively financial expenses and calculate what proportion of income represents EBITDA (operating income plus depreciation and amortization) the main financial indicator of the internal generation of funds and EL EVA indicator of value creation, fairly representative when corporate governance is evaluated and when a company is valued.

An important complement to analyzing the income statement is the cost of capital, which given its importance should be kept under control using a dynamic model that keeps you updated on the indicator as a reference for negotiations and credit acquisition, development, and provision of financial savings, supplier selection and changes in the financial structure, verifying that the principle of conformity to be respected. The resulting statement is to calculate the activity indicators that make up the complement of liquidity indicators.

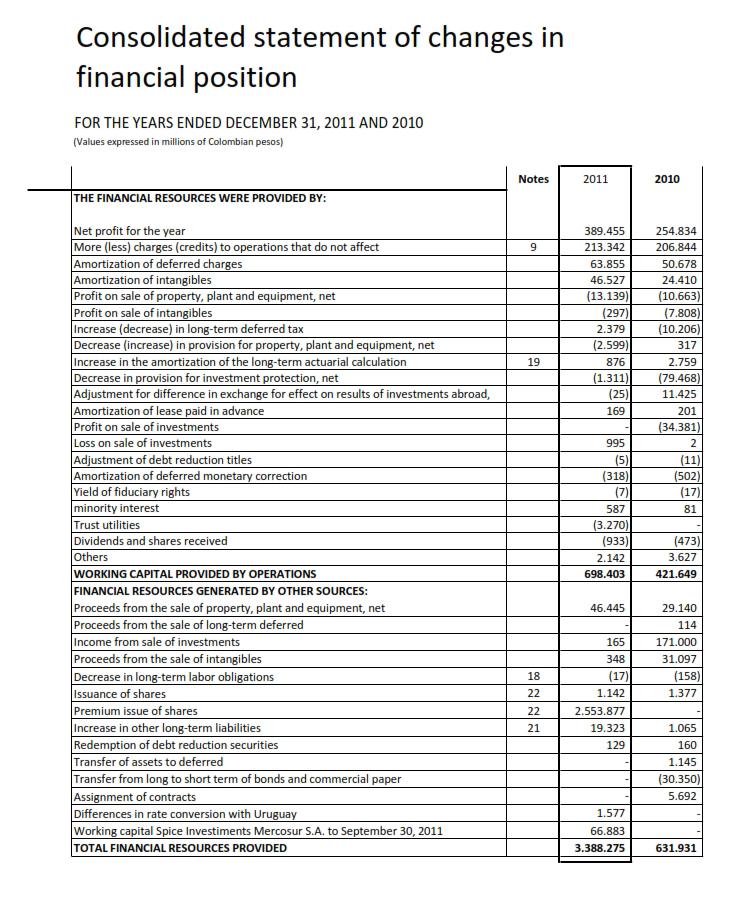

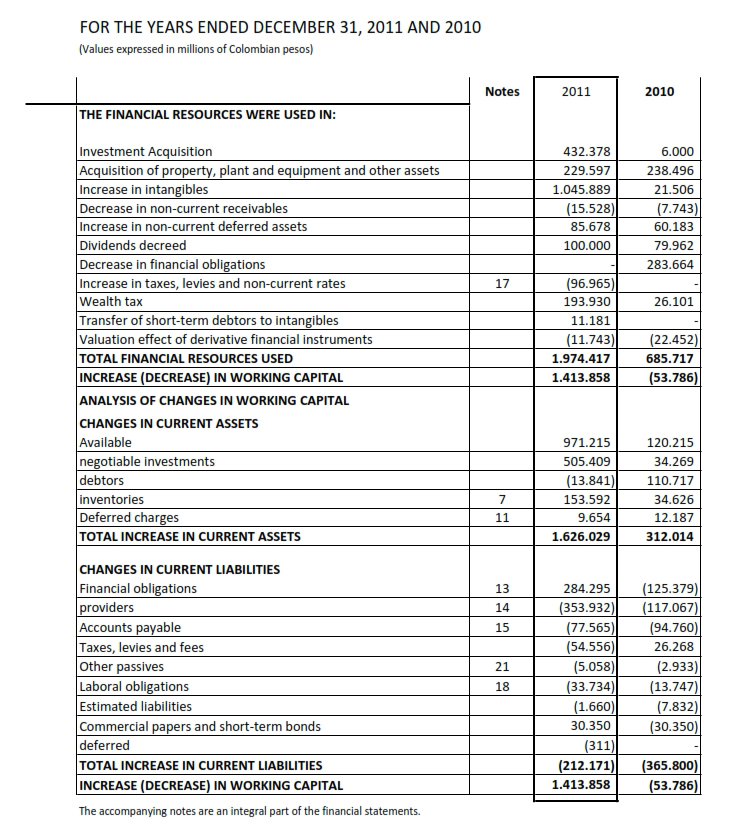

3. STATEMENT OF CHANGES IN FINANCIAL POSITION

Used to calculate changes in net working capital by definition equal to the difference between assets and current liabilities, comparing baseline with the end of a period, to determine whether increased or decreased provided; is used to analyze where the cash was obtained and was used, which makes it the ideal place to verify compliance with the principle of financial compliance tool.

Any reduction of an asset or a liability increase is a source of funds. Logically, any increase in assets or a decrease in liabilities is the use or application of funds. Does it answer questions like what revenues from the sale of land were used? What was done with the cash and the issuance of shares with money from bond issues in the market? It also serves as a good tool for checking the plans for financing investments and dividend payments without affecting the equity of the company.

Sources of cash companies are:

a) internally, generated cash include profits of the period plus depreciation and amortization because the latter do not represent cash outflows but profits fell in the proportion that was recorded in the cost of goods sold to calculate the income for the period.

b) The liquidation of investments if they arise.

c) Loans to short and long term

d) the sale of assets, a situation that eventually may have.

It is recommended, before approving the development plan of the company verify the statement of changes in financial position projected if funding sources are recommended to preserve an adequate structure respecting the principle of conformity and, if it is necessary, make timely corrections

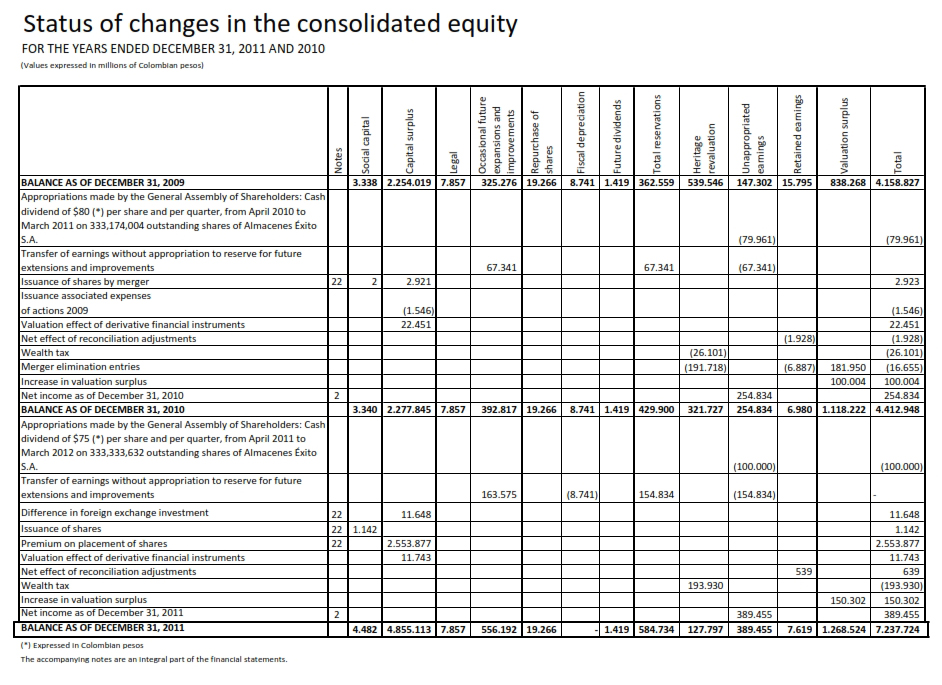

4. STATEMENT OF CHANGES IN EQUITY

The estate consists of contributions from owners retained earnings from previous periods and exercise, reserves, revaluation surplus, the revaluation of assets, additional paid-in shares, and donations.

Prepare for a period and enables the detail that heritage and how heritage started over. Ideally, its value is increased by way of creating value with good liquidity to meet development.

The capital subscribed and paid corresponds to the capital actually invested by the partners; surplus corresponds to the increase made in the ordinary operation of the business profits of the period plus earnings from previous periods undivided (fewer losses and prior period ) and other asset increases the social object such as paid in shares.

Reservations are part of the profits that are used for a specific purpose. The legal reserve is required to protect the heritage character and represents 10 % of the net profits of each year to complete at least 50% of the subscribed capital. They can also be statutory and occasional.

The revaluation of assets reflects the value of the inflation adjustments.

The respective accounts of the balance for all accounting purposes until paid are the depreciation and the amortization. The balance of the equity revaluation account may be reduced with the departure tax of cleared heritage and cannot be distributed as income until the liquidation of the company.

Net assets serve as measuring the generation of value as a higher return on equity than the cost of capital, which of course should be calculated taking into account the contribution of the partners has an equivalent cost is achieved the best alternative that offers the market; also to calculate the intrinsic value of the share, compared to standard market value.

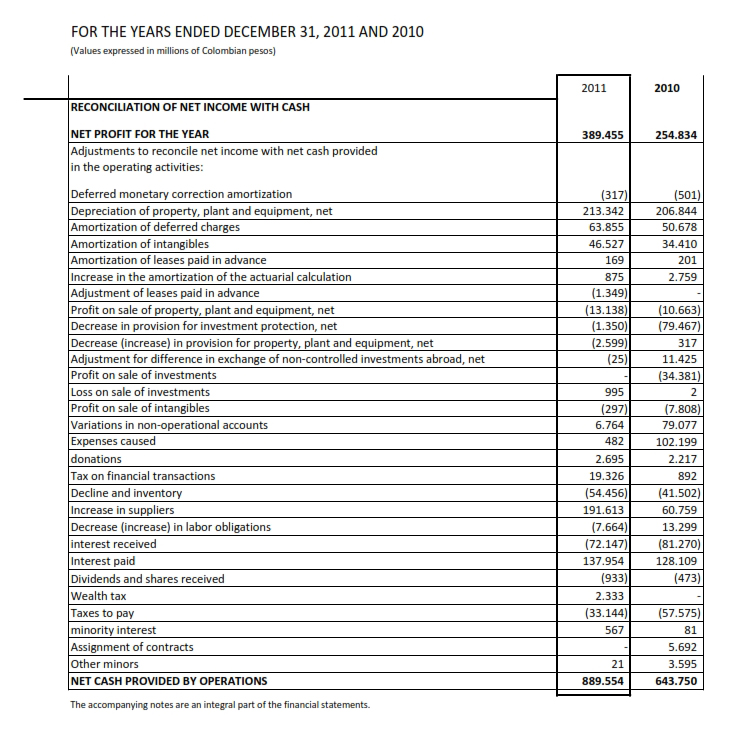

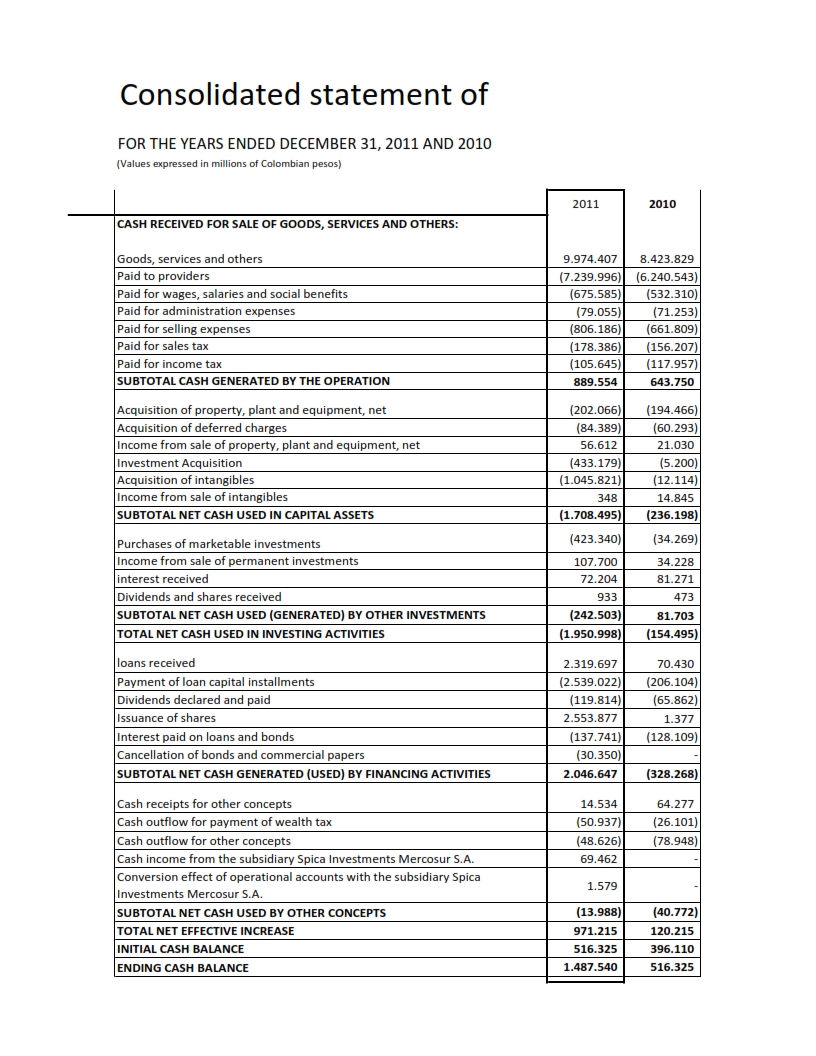

5. CASH FLOW STATEMENT

Prepare for a period and show net income and payments of any kind, starting with the ending balance of the previous period (figure balance) and ending with the final balance, which is equivalent to the amount of closure. It is the most powerful financial tool to observe the periodic resource generation after fulfilling its commitments relates to the basic function of the financial executive. Its preparation is very simple because it merely records the facts as they are presented in a predetermined format, differing operating, investing, and financing.

For purposes of presentation to stakeholders can be done by an indirect method commencing with the net figure income statement and adding or deducting items not involving the receipt or payment of cash, namely depreciation, amortization, and depletion; provisions, Exchange rate differences and gains or losses on the sale of fixed assets and investments.

To be of real help as a financial instrument should be designed to exercise separating domestic and from operating income of foreign operations of non-operating income on the dates that are expected to receive, based on the policies of sales (cash and credit) and accumulated experience. The total equals 100% which should decompose concepts and monthly figures to collect and maintain the cumulative figures.

Expenses, for administrative purposes, should be decomposed into :

a) Tax,

b ) Labor,

c ) Operating ( everything needed to operate the plant).

d ) Suppliers.

e) Banks and financial institutions.

Whose sum represents the total of cash outflows, a figure projected to be periodically and on a cumulative percentage, and breaking to see the relative importance of each?

Dividing the sum of total operating expenses for the number of working days which gives cash worth a day, a figure very important managerially speaking, to calculate the amount that the company must keep available to meet the expenditure to operate; value equivalent to cash a day by the number of days in the operating cycle.

It is very important to note that projected cash flow is the result of a financial planning process that constitutes the top of a value creation plan, a fundamental tool for good governance.

IA Opinion: The work "Financial Information for Analysis and Decision Making" by José Saúl Velásquez Restrepo presents a comprehensive and detailed vision of the importance of financial information in the modern business context. Below is an opinion on the main topics addressed:

1. Context of the Fourth Industrial Revolution: The author establishes an important connection between changes in the business environment, including the Digital Revolution and the COVID-19 pandemic, and the need to adapt financial and business models to maintain competitiveness . This updated and contextualized vision is essential to understand the challenges and opportunities that companies face today.

2. Focus on Sustainability and Social Responsibility: The importance of companies not only seeking financial profitability, but also considering the social and environmental impact of their operations is highlighted. This focus toward “conscious capitalism” reflects a growing trend in the business world toward corporate social responsibility and sustainability.

3. Importance of Financial Education: The author emphasizes the need for all people, regardless of their profession or trade, to acquire basic knowledge in finance and accounting. This is essential for financial decision making at both a business and personal level, reflecting the importance of financial literacy in society.

4. Practical Aspects of Accounting: A detailed explanation of accounting principles and financial statements is provided, which may be useful for those seeking to better understand accounting terminology and concepts. In addition, practical examples and recommendations for financial analysis are provided, which can be valuable for professionals in the financial field.

5. Emphasis on Transparency and Business Ethics: The importance of transparency in the presentation of financial information is highlighted and ethical business practices are advocated. This ethical approach is crucial to building trust among investors and other stakeholders, and to promoting stability and integrity in financial markets.

3. Statement of Changes in Financial Situation:

· You offer a clear explanation of how this statement helps understand changes in net working capital, which is essential for evaluating the financial health of a company.

· The distinction between sources and uses of funds is crucial and provides clear examples of each.

· The recommendation to verify financing sources before approving the company's development plan is correct and shows a deep understanding of the importance of financial planning.

4. Statement of Changes in Assets:

· Your explanation of the components of heritage is detailed and easy to understand.

· Highlighting the importance of increasing the value of assets and its relationship with the generation of value is accurate and shows a strategic vision.

· The explanation of reserves, both legal and statutory, is useful to understand how profits are managed in a company.

5. Cash Flow Statement: You clearly explain the importance of the cash flow statement as a fundamental financial tool and its usefulness to understand the periodic generation of resources.

· Breaking down income and expenses by category is useful for understanding where the company's cash comes from and where it goes.

· Highlighting the importance of projected cash flow as a result of financial planning is essential and shows a deep understanding of financial management.

Overall, the work provides a complete and up-to-date view of the importance of financial information in the contemporary business world, as well as practical guidance for those interested in understanding and applying financial concepts in decision making.

The second part of your opinion addresses crucial aspects of the financial management of a company, specifically the Statements of Changes in Financial Situation, Equity and Cash Flows. Here is a review and additional comments:

Overall, your opinion demonstrates a solid understanding of key financial principles and provides useful guidance for the financial management of a company.